Introduction

U.S. presidential elections don’t just affect politics: they also strongly influence financial markets.

Our study “American Elections and Financial Markets: In-Depth Analysis of Trends Since 1988” revealed that, right after an election, small and mid-cap equities (also called SMC capitalizations) tend to outperform large-cap stocks, including those in the technology sector.

Following Donald Trump’s victory in 2024, this trend is confirmed with what is known as the “Trump Rally.”

In this article, we explain the reasons behind this dynamic in clear terms, analyzing causes and effects.

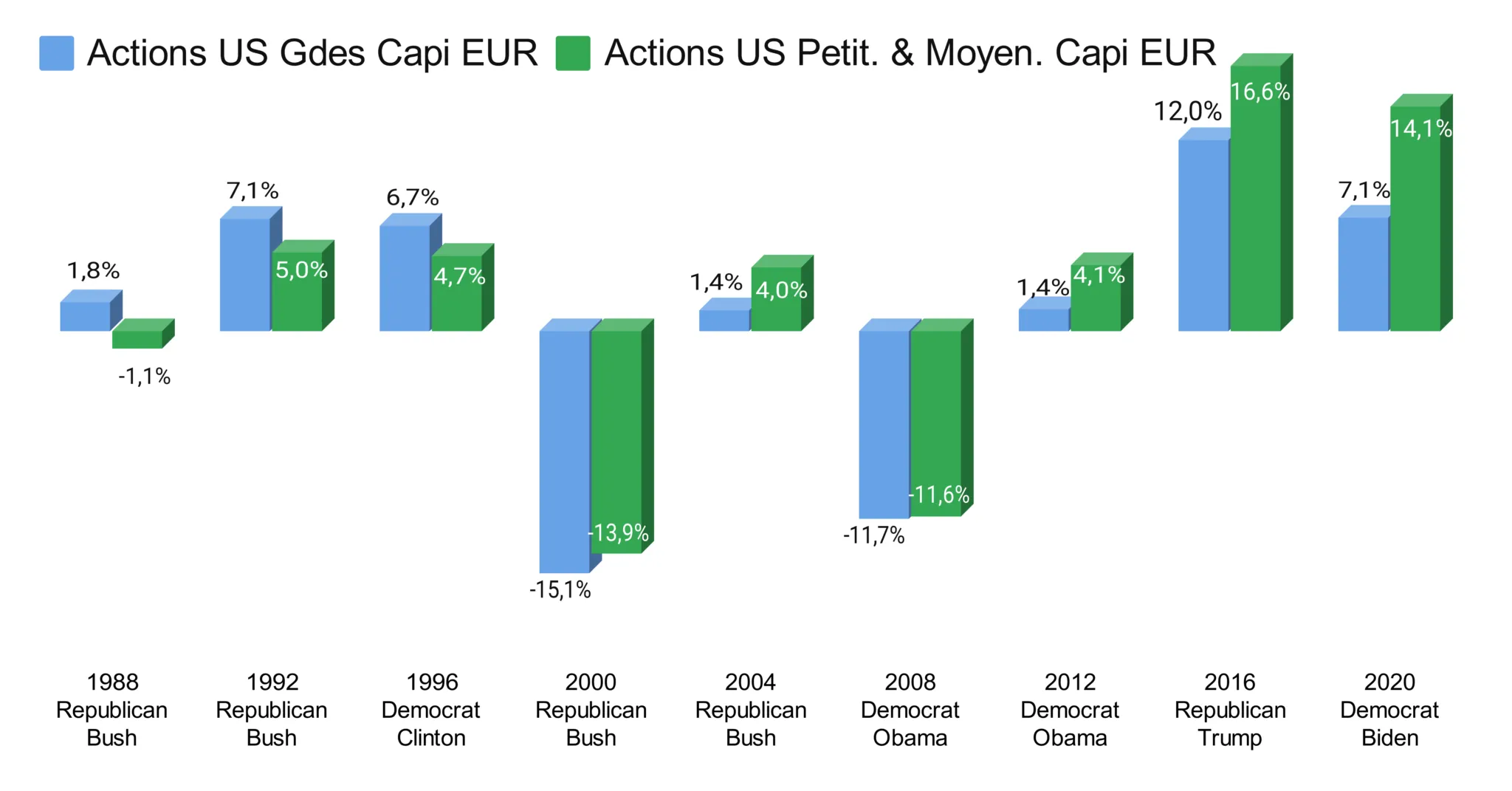

2-Month Post-Election Performance

Performance from November 4 to 8, 2024

1. Strong Dollar Effect: An Advantage for Domestically Focused Companies

What is happening: After an election, changes in economic policy often influence the national currency’s exchange rate. Following Donald Trump’s victory, the dollar strengthened, meaning it is now worth more relative to other currencies, such as the euro or yen.

Why it matters: A strong dollar can penalize large American companies that sell heavily abroad. When they convert their foreign currency revenues into dollars, they get fewer dollars for the same sale, which reduces their consolidated earnings. This effect weakens their position on the stock market.

Who benefits: Conversely, small and mid-sized companies are often more focused on the American market and are therefore less affected by this conversion effect. On the contrary, they benefit from it: a strong dollar allows them to import raw materials at lower cost, thereby improving their profit margins. In short, they become more profitable and thus attract investors.

2. Style Rotation: SMEs Become More Attractive

What is happening: Over the past decade, large companies, particularly those in the technology sector, have experienced meteoric growth. These companies have become very popular and their stocks are now expensive relative to their earnings.

Why it matters: After an election, investors reassess their portfolios and look for buying opportunities at more attractive prices. This is where SMEs come into play: they are cheaper because they have not yet benefited from the same enthusiasm as large caps.

Who benefits: Small and mid-sized companies thus become a preferred target for investors seeking growth potential, especially in an economic environment focused on the domestic market. This style rotation drives a flow of capital toward these SMEs, which then benefit from increased demand for their stocks, and therefore a rise in their market value.

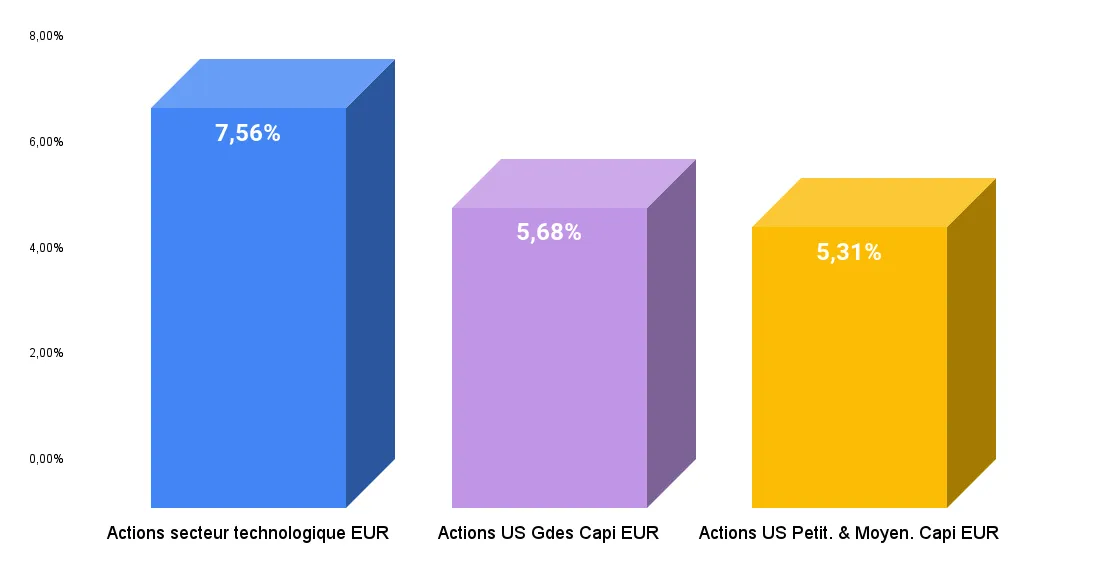

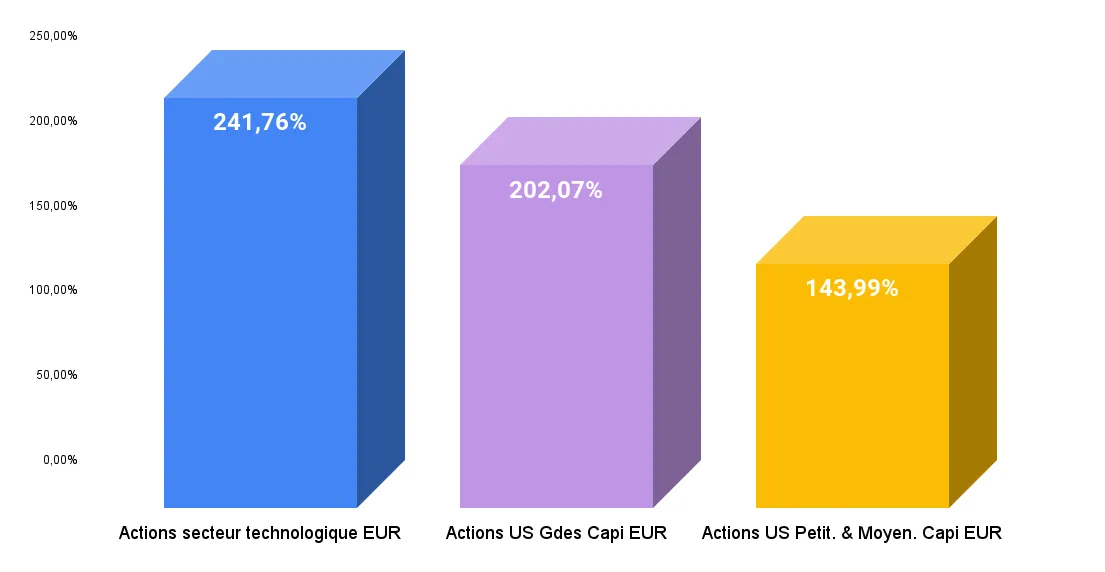

Performance from November 7, 2014 to November 7, 2024

3. Yield Curve: A Favorable Configuration for SMEs

What is happening: Interest rates play a key role in corporate financing. In the United States, the Federal Reserve sets short-term interest rates, while long-term rates are determined by the market. The yield curve, that is, the difference between short-term and long-term rates, indicates how investors perceive the economy.

Why it matters: Small and mid-sized companies often depend on short-term loans to finance their operations. When short-term interest rates are low, as is currently the case, these SMEs can borrow at lower costs, enabling them to grow more easily.

Conversely, large companies, which often invest in large-scale projects such as research and development, are sensitive to long-term rates. Low long-term rates allow them to finance these projects at lower cost. Currently, however, long-term rates are elevated, which complicates this type of investment for large companies.

Who benefits: In the current 2024 context, with declining short-term rates and higher long-term rates, small and mid-sized companies find themselves in a position of strength. They benefit from low short-term borrowing costs and can take advantage of domestic growth prospects, while large companies face higher financing costs for their long-term projects.

4. How Long Can This Outperformance Last?

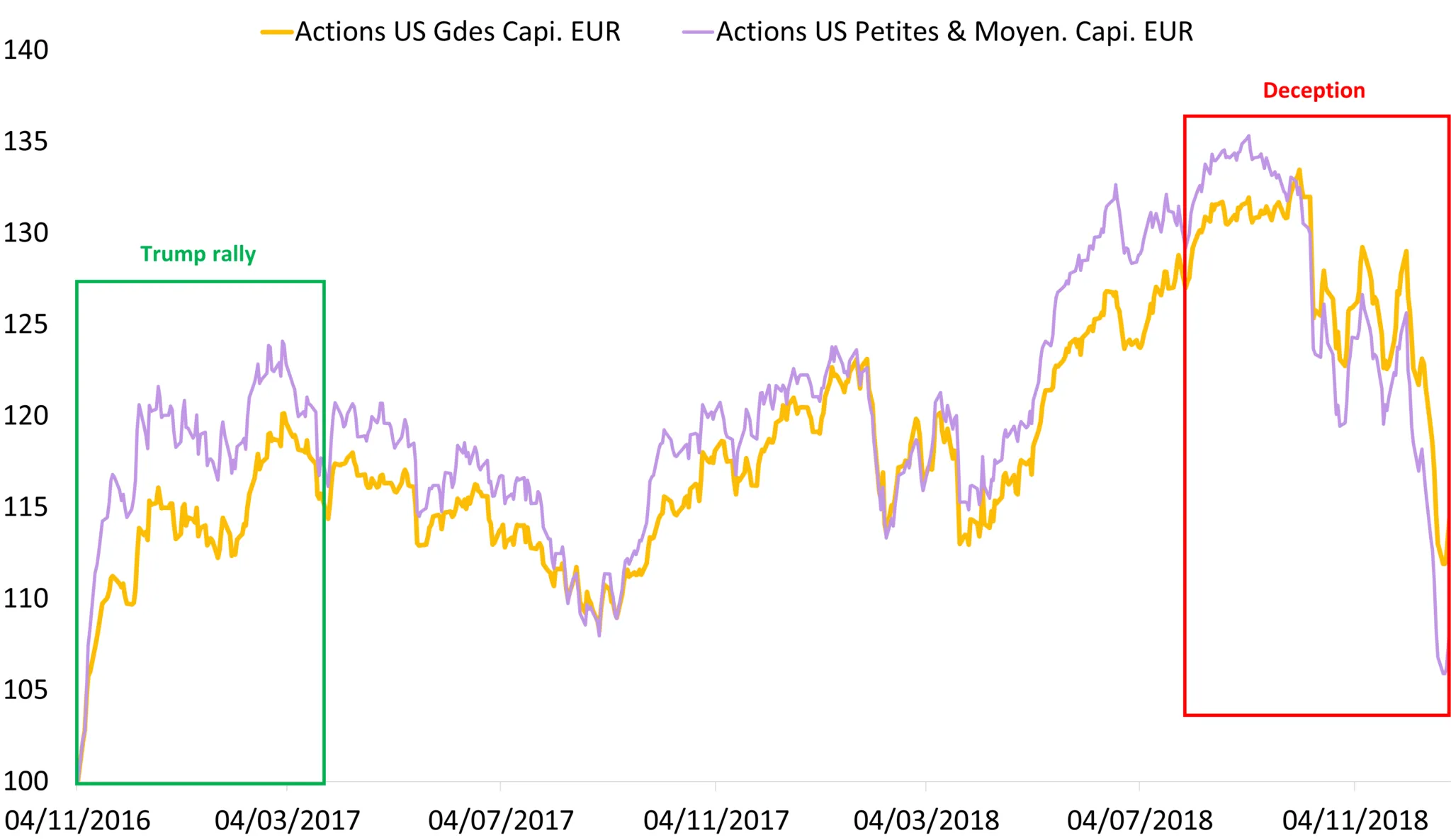

Data shows that post-election effects can last several months. For example, after Trump’s first election in 2016, small and mid-cap stocks outperformed for more than 4 months. However, these expectations are largely based on the anticipated economic policies of the Trump administration.

It is important to note that in 2016, Trump had promised to invest massively in infrastructure, but this promise was not kept. The market was disappointed and subsequently penalized Small and Mid-Cap Equities.

Investors will therefore closely monitor the concrete measures implemented by the new government. The market’s reaction will depend on the effective realization of these promises, which could influence the duration of small and mid-cap outperformance.

Trump Rally 2016 Performance

5. Currency Effect for European Investors

What is happening: European investors who invest in the U.S. market directly benefit from the dollar’s rise against the euro. Indeed, a strong dollar enhances the euro-denominated gains of a dollar-based investment.

Why it matters: When a European investor places funds in dollars, their gains increase if the dollar appreciates against the euro. For example, an investment in U.S. equities that returns 8% in dollars generates an even higher return in euros if the American currency appreciates against the euro.

Numerical Example: Suppose a European investor places 100,000 euros in American SME equities, with an 8% performance in dollars. If the dollar gains 5% against the euro, the total return in euros would be 13%, representing a gain of 13,000 euros (8,000 euros in market performance and 5,000 euros in currency effect), instead of only 8,000 euros without the currency effect.

Note for European investors: To maximize this double effect (U.S. market performance and exchange rate advantage), it is preferable to choose unhedged euro share classes of funds in the US Small and Mid-Cap Equities category. An unhedged share class allows you to fully benefit from the currency effect, unlike euro-hedged share classes that neutralize this effect.

For ETFs, verify whether the tracker is composed of physical equities rather than derivatives. Trackers based on physical equities directly hold the securities in their portfolio, which provides more faithful exposure to the underlying market and embeds the currency risk.

Conclusion

The 2024 American elections reinforce the outperformance dynamic of small and mid-cap stocks, driven by clear and identifiable factors: a strong dollar, a favorable short-term financing environment, and attractive valuations. Analysis of historical data and market fundamentals shows that SMEs have strong arguments for continuing to dominate in this context.

However, investors will need to remain attentive to the concrete measures taken by the administration to verify whether current expectations materialize.

EnvestBoard offers advanced analytical tools to explore these dynamics and understand how to optimize investment portfolios based on market data.

About the author: Yufeng Xie is the CEO and co-founder of EnvestBoard, an innovative investment decision-support platform.