Consumer Sector Category

Overview

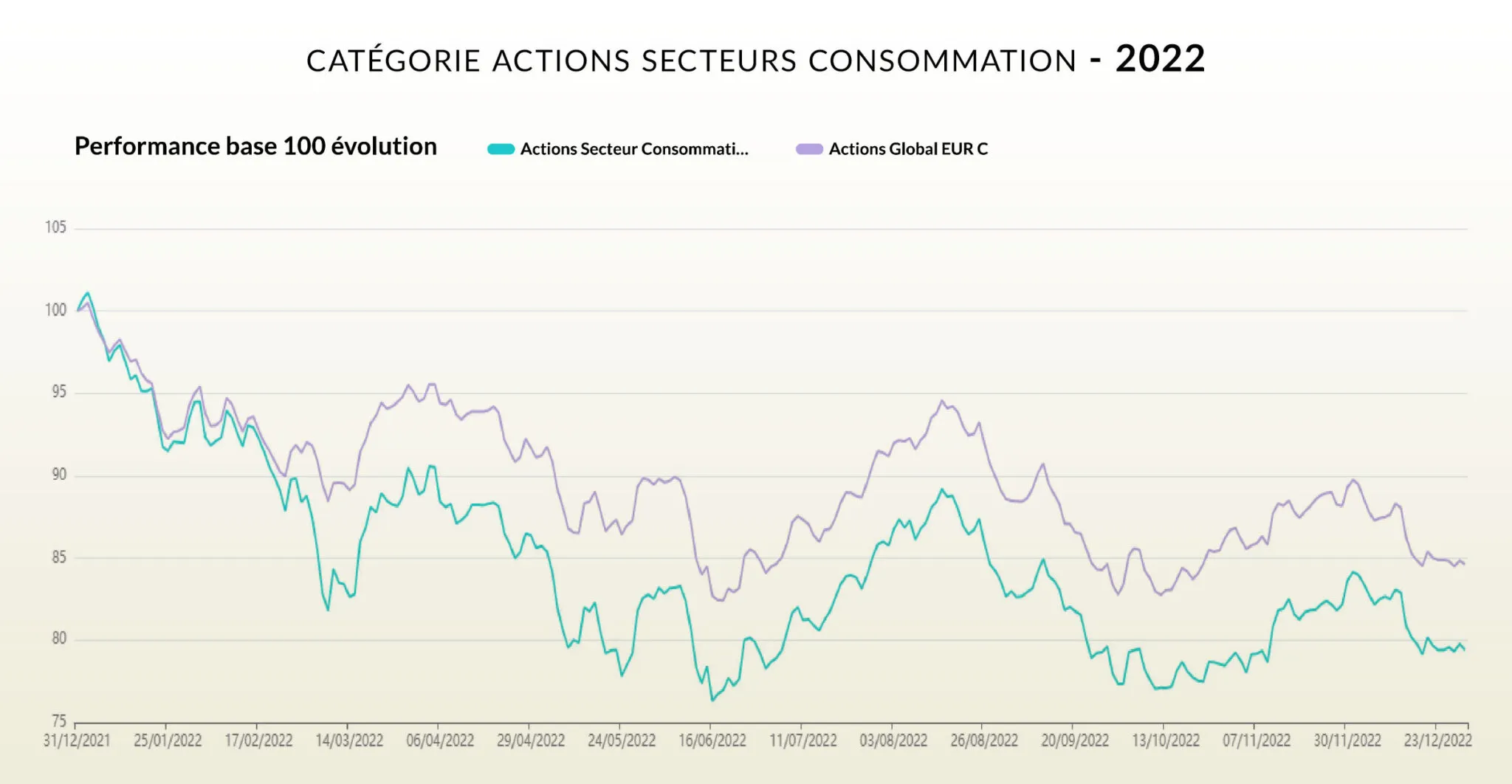

- The sector suffered during 2022 with successive rate hikes and the closure of China

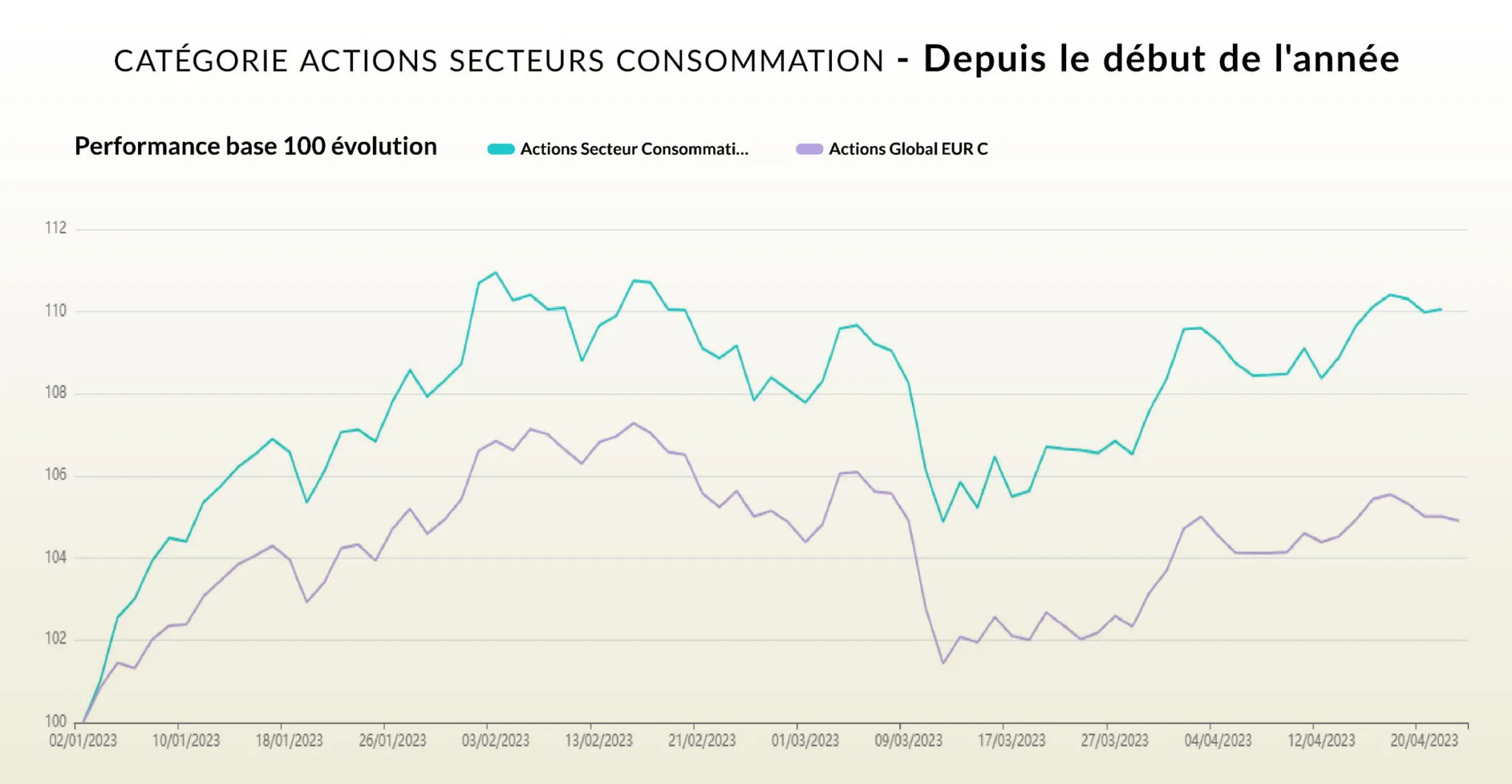

- The reopening of China boosted the sector, driven by its luxury segment

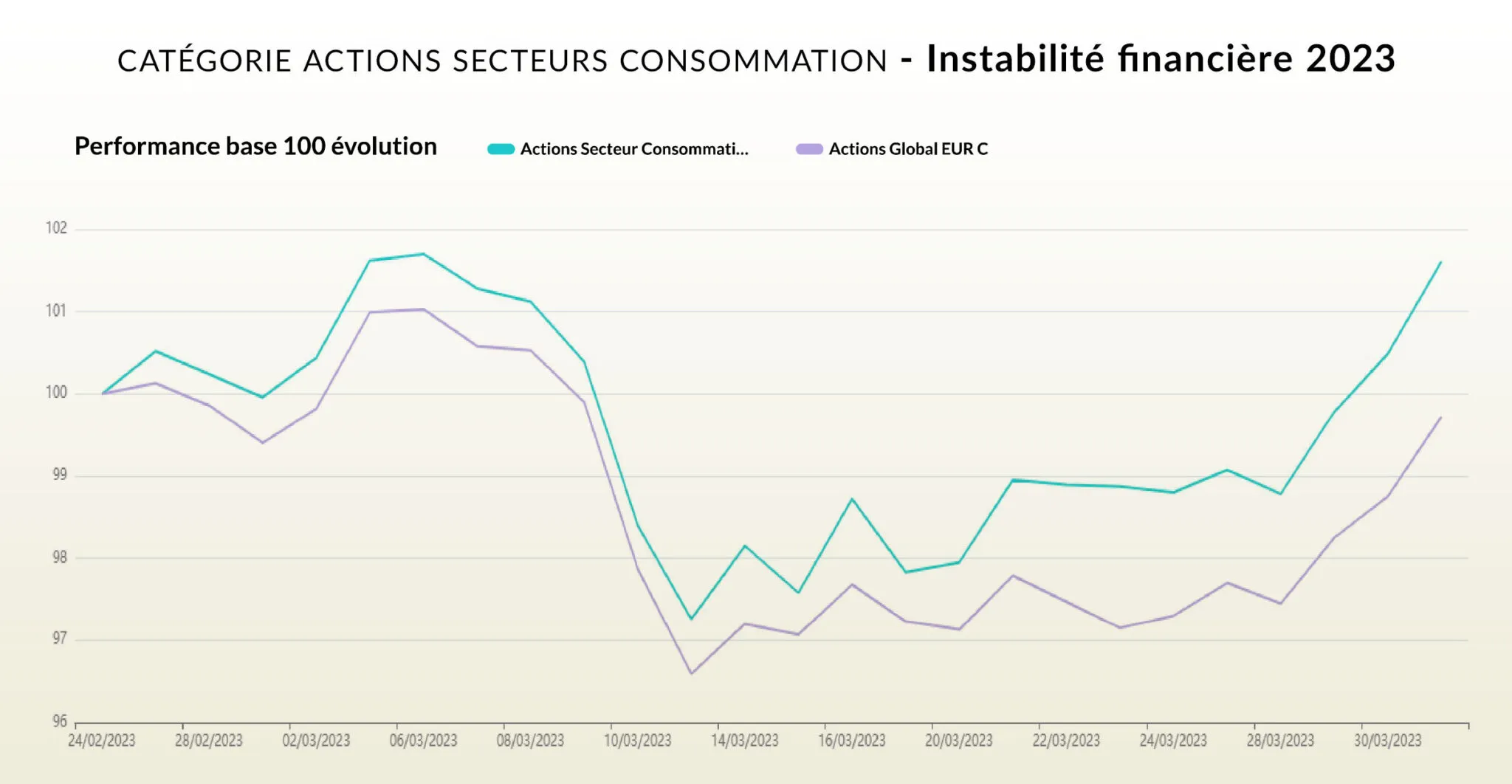

- The sector suffered less than its peers during the financial instability at the start of this year thanks to strong consumer spending figures

Current Situation

The sector benefits from several macroeconomic factors. Indeed, despite successive rate hikes and inflation, global consumer spending is weakening but remains positive. Moreover, the rebound of the Chinese economy could be stronger than expected.

Financial system instability raised the risk of a significant recession. This reminds us that we are still navigating an unstable economic environment. In this climate, the sector has been more resilient than the broader equity market and shows significant resilience at the start of this year.

Scenarios

Optimistic

If central banks continue to stabilize or even slow inflation without aggressive rate hikes and the Chinese rebound accelerates, the sector could maintain its very positive trend since the beginning of the year. It could even receive a boost if the Fed does not raise rates or even reverses its monetary policy.

Pessimistic

Caution is warranted as it is not impossible for the trend seen at the start of this year to reverse. Indeed, inflation appears stabilized, but several rate hikes can be envisioned to continue maintaining it at an acceptable level. Moreover, Sino-American tensions could dampen the Chinese rebound due to trade and economic frictions. In this scenario, we could face a significant decline in the sector as we experienced in 2022.

Past performance is not indicative of future results. Fees are included in performance figures. The content above does not constitute investment advice. It is an objective analysis of financial information.