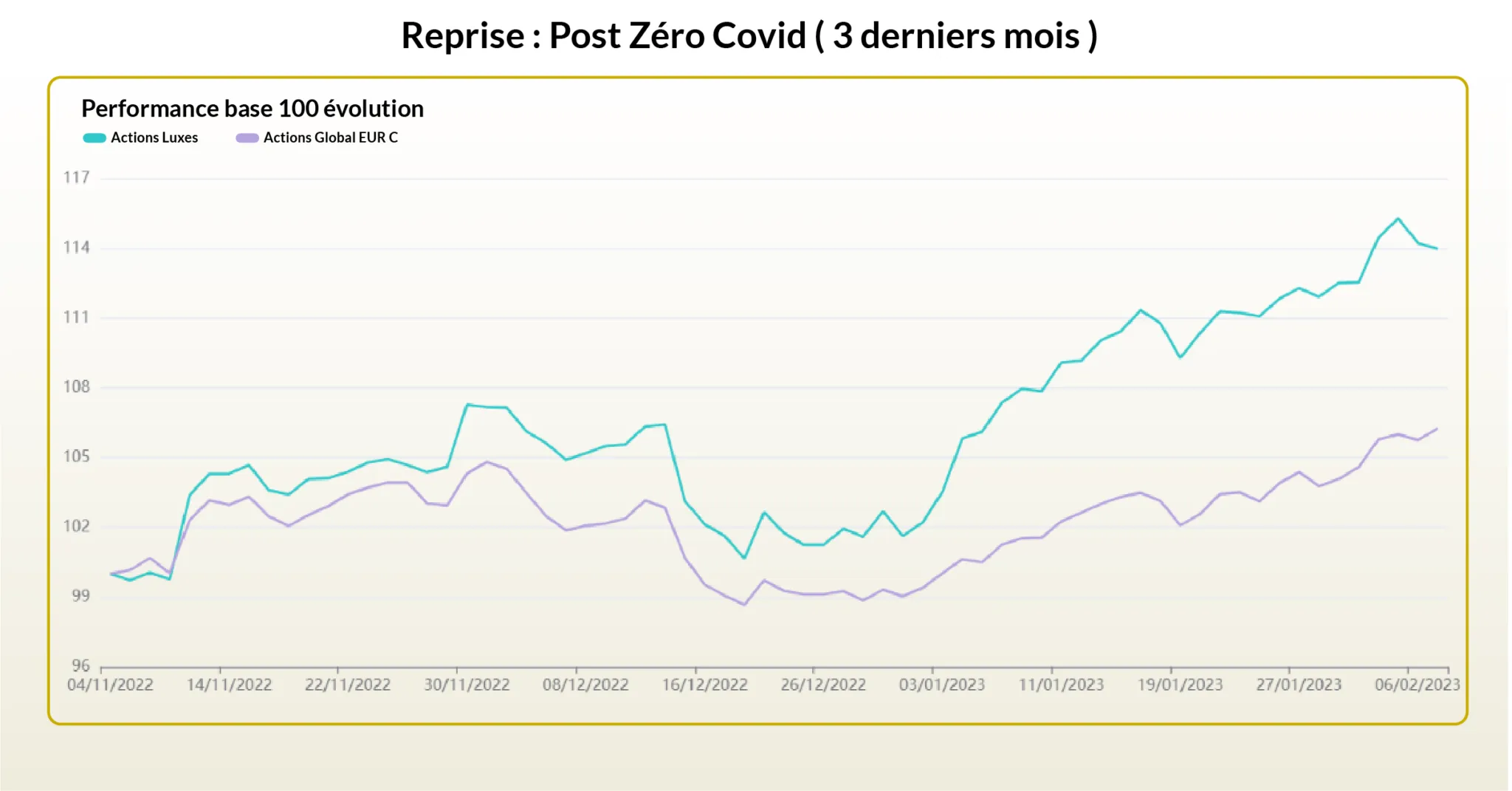

Overview

- Europe is the epicenter of luxury worldwide. The sector is a remarkable success story for the old continent: 10% of its exports, 3% of its GDP (not counting the tourism it generates) and 1.5 million jobs

- However, being both a local and global business, the luxury sector was hit hard in 2022 by China’s Zero Covid policy. China has been the main driver of growth for the sector in recent years

The average performance of Luxury funds was -15% during 2022.

Current Situation

- Currently, China’s reopening offers a better macro outlook for the sector

Scenarios

Positive Scenario

China’s reopening would improve the macro outlook for the sector.

Furthermore, in a world where inflation is high but under control, luxury companies could gain investor preference due to their ability to pass on price increases. Indeed, they have both significant margins and a customer base that is less sensitive to inflation. This scenario appears to be favored by the market in the short term.

Negative Scenario

Given the limited transparency of CCP governance in China, it is not impossible that the reopening situation may be volatile in the coming months. This could undermine the still fragile recovery of confidence in the sector, and we could see a rise in volatility similar to 2022.

Past performance is not indicative of future results. The content above does not constitute investment advice. It is an objective analysis of financial information.