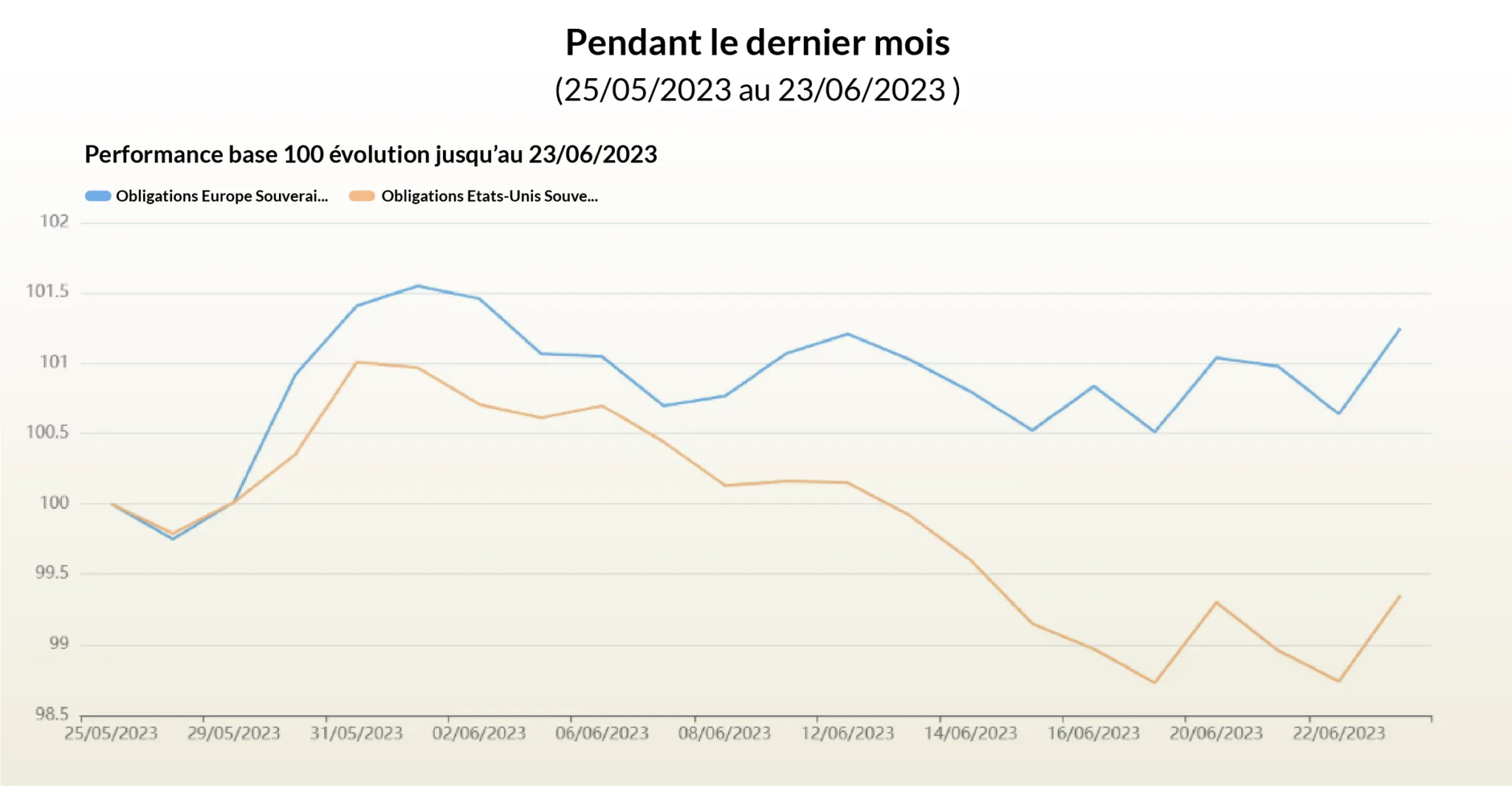

Overview: The Divergence of Economic Dynamics Between Europe and the United States

The recent publication of macroeconomic indicators reveals a certain fragility in industrial activity in Europe, while in the United States, employment and other leading indicators maintain their robustness. This divergence in economic dynamics could lead to a split in the upcoming policies of the Federal Reserve (Fed) and the European Central Bank (ECB). If this trend were to be confirmed, the Fed would likely be compelled to continue raising interest rates, while the ECB could adopt a more patient stance.

In this context, we can envision two scenarios for this divergence.

Scenario 1: The Fed Accelerates Rate Hikes — Impact on European Sovereign Bonds

There are many potential reasons explaining the slowdown in industrial activity in Europe. It could be temporary, caused by rate hikes from the ECB, or due to a lack of dynamism in international trade. Europe, as the most open economy, is highly sensitive to the evolution of global trade, which currently presents challenges. For the same reason, Europe may not experience lasting inflationary pressure.

Conversely, the United States, as a more closed economy, could be less sensitive to changes in the global economy. It faces more persistent inflationary pressure, supported by the robustness of domestic demand. In this hypothesis, European sovereign bonds could constitute a good diversification instrument: they would face less inflationary pressure and offer protection against the real economic slowdown expected by the market.

Scenario 2: The European Rebound — the ECB Forced to Follow the Fed

Given current uncertainty, it is difficult to rule out that the observed slowdown is merely temporary. If that were the case, the market would anticipate that the ECB would be forced to follow the Fed in raising rates. In this scenario, European sovereign yields would once again come under pressure, as we observed between Q1 and Q3 2022.

Past performance is not indicative of future results. Fees are included in performance figures. The content above does not constitute investment advice. It is an objective analysis of financial information.